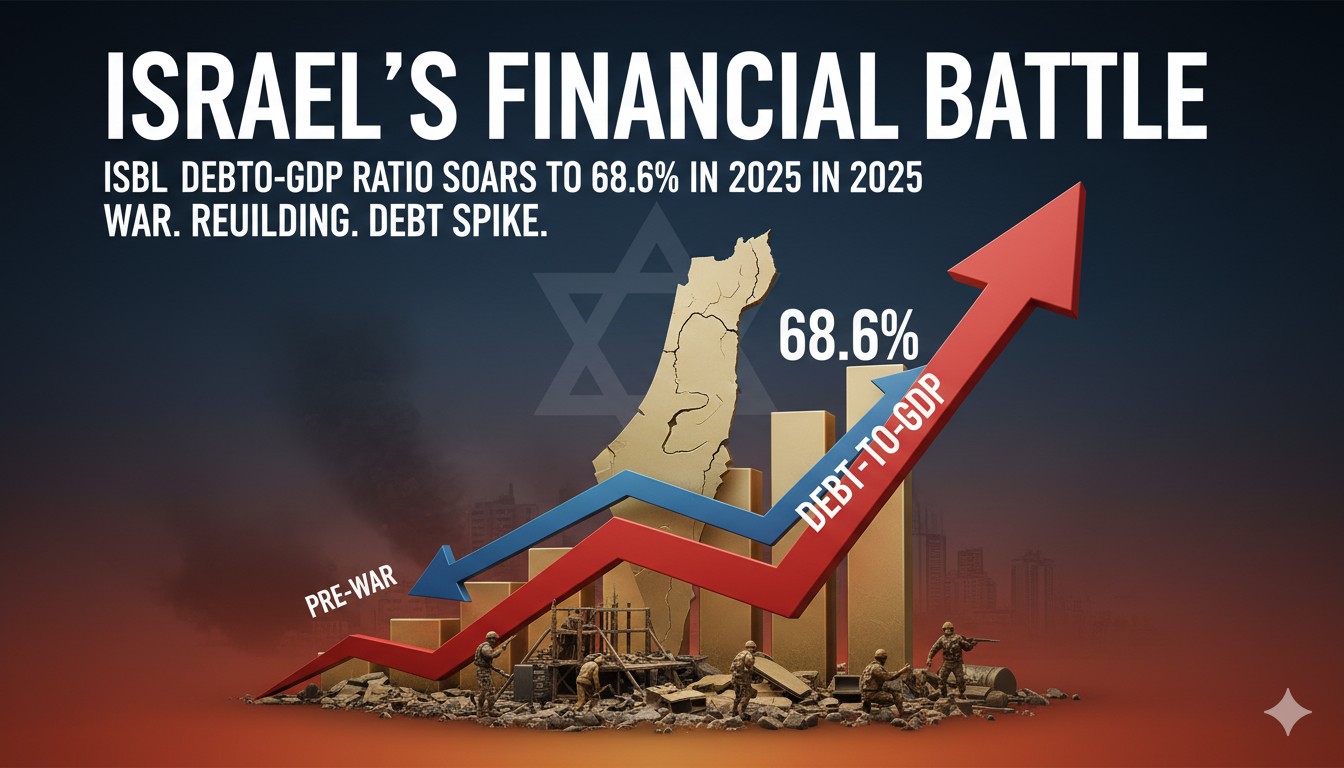

Israel’s public debt-to-GDP ratio increased to 68.6% by the end of 2025, driven by substantial war expenditures and reconstruction efforts, marking a rise from 67.7% in 2024. The government allocated over NIS 90 billion to military operations and related activities, contributing to a budget deficit of 4.7% of GDP, equivalent to NIS 98.6 billion. Economic growth slowed to around 1%, with sectors like tourism, construction, and exports facing disruptions, while inflation remained above targets and credit ratings experienced downgrades. Fiscal strategies include potential tax adjustments and spending reallocations to stabilize the trajectory.

Economic Overview Israel’s fiscal landscape in 2025 reflected the profound pressures from ongoing military engagements and the imperative for post-conflict recovery. The debt-to-GDP metric, a critical indicator of fiscal health, edged up to 68.6%, underscoring the strain on public finances. This uptick stemmed primarily from heightened defense outlays, compensation for affected civilians and businesses, and infrastructure rebuilding in conflict-impacted regions. War-related spending alone surpassed NIS 90 billion, encompassing direct military costs, reservist mobilizations, and aid to displaced populations. These expenditures amplified the budget deficit to 4.7% of GDP, totaling approximately NIS 98.6 billion, far exceeding initial projections that anticipated a more contained shortfall.

The broader economic ramifications extended beyond debt metrics. GDP growth decelerated to about 1%, a stark contrast to pre-war forecasts that envisioned expansion closer to 3-4%. Key drivers of this slowdown included labor shortages from reservist call-ups, which affected nearly 300,000 workers at peak times, and supply chain interruptions in high-tech and manufacturing sectors. Inflation hovered above the central bank’s 1-3% target range, averaging around 3.5% for the year, fueled by rising energy prices and import dependencies amid regional instability. Unemployment ticked up to 4.2%, with particular impacts in border areas and industries reliant on cross-border trade.

| Year | Debt-to-GDP Ratio (%) | Key Contributing Factors |

|---|---|---|

| 2023 | 60.0 | Pre-war stability with controlled spending |

| 2024 | 67.7 | Initial war escalation and emergency funding |

| 2025 | 68.6 | Sustained military operations, rebuilding, and deficit expansion |

Impact of War on Key Sectors The protracted conflicts exerted multifaceted pressures across Israel’s economy. In the defense and security domain, expenditures ballooned to cover advanced munitions, intelligence operations, and border fortifications. Estimates peg the cumulative war costs from 2023 through 2025 at over $55 billion, representing roughly 10% of GDP over that period. This included $14 billion in supplemental funding for 2024-2025, directed toward missile defense systems and troop deployments. Rebuilding expenses added another layer, with allocations for repairing damaged infrastructure in southern and northern regions exceeding NIS 20 billion. Residential reconstruction, public facility repairs, and agricultural rehabilitation in conflict zones further inflated these figures, as insurance claims and government subsidies surged.

Tourism, a vital revenue stream contributing about 3% to GDP pre-war, plummeted by 80% in 2025. International visitor numbers dropped to under 1 million, compared to over 4 million in peak years, due to travel advisories and flight cancellations. This ripple effect hit hospitality, retail, and transportation, leading to widespread business closures and layoffs. Construction activity contracted by 15%, hampered by material shortages and labor diversions to military needs. Exports, which account for 30% of GDP, declined by 8% year-over-year through October 2025, with high-tech shipments resilient but diamond and chemical exports suffering from global boycotts and logistical hurdles.

Agriculture faced acute challenges, with farmland near borders rendered unusable, resulting in a 20% drop in output for crops like fruits and vegetables. Energy sectors contended with heightened risks to offshore gas fields, prompting increased imports and price volatility. The shekel depreciated by 5% against the dollar over the year, reflecting investor caution and capital outflows estimated at $10 billion. Credit rating agencies responded with downgrades: Moody’s shifted Israel’s outlook to negative, citing fiscal vulnerabilities, while Fitch highlighted risks of prolonged deficits pushing debt beyond 70% if conflicts persist.

Fiscal Measures and Policy Responses To counteract these pressures, policymakers implemented a series of adjustments. The central bank maintained interest rates at 4.5% through much of 2025, prioritizing inflation control over stimulus, though signals emerged for potential cuts if growth stalled further. Rate decisions were influenced by persistent inflationary trends from war-induced supply shocks. On the fiscal front, the government revised the 2025 budget to incorporate war contingencies, reallocating funds from non-essential areas like cultural programs to defense and welfare. Tax measures included temporary hikes in value-added tax on luxury goods and corporate surcharges for defense firms, aiming to generate an additional NIS 15 billion in revenue.

Debt management strategies focused on diversifying borrowing sources. Israel issued $8 billion in international bonds, attracting U.S. and European investors despite higher yields of around 4.5%. Domestic bond sales covered another NIS 50 billion, supported by institutional buyers like pension funds. Efforts to curb the deficit involved expenditure caps, freezing new hires in public sectors unrelated to security, and deferring infrastructure projects outside conflict zones. International aid played a stabilizing role, with annual commitments of $3.8 billion supplemented by emergency packages, bolstering reserves that stood at $220 billion by year-end.

Key Fiscal Adjustments in 2025 :

Defense budget increased by 30% to NIS 120 billion.

Welfare spending rose 15% for evacuee support and business grants.

Revenue enhancements via targeted taxes yielded NIS 10-15 billion.

Bond issuances financed 40% of the deficit.

Future Outlook and Risks Projections for 2026 anticipate the debt-to-GDP ratio stabilizing around 68-70%, contingent on de-escalation. If military operations extend, estimates suggest an additional 0.5% GDP contraction and debt climbing to 71%. Growth recovery hinges on sector-specific rebounds: high-tech, comprising 15% of GDP, could drive 2-3% expansion if global demand holds, but persistent boycotts pose threats. Inflation is forecasted to ease to 2.5% with normalized supply chains, though energy risks remain.

Budgetary discipline will be pivotal, with proposals for a multi-year framework capping deficits at 3% of GDP. Structural reforms target labor market flexibility, including retraining programs for reservists and incentives for foreign workers to fill gaps in construction and agriculture. Geopolitical uncertainties, including potential escalations with regional actors, could exacerbate outflows and rating pressures. Conversely, peace dividends might unlock investments in innovation hubs, potentially boosting productivity by 1-2% annually.

Risk Factors :

| Projected Scenarios for 2026 | Debt-to-GDP (%) | GDP Growth (%) | Deficit (% of GDP) |

|---|---|---|---|

| Baseline (De-escalation) | 68.5 | 2.5 | 3.0 |

| Prolonged Conflict | 71.0 | 1.0 | 5.0 |

| Accelerated Recovery | 67.0 | 3.5 | 2.5 |

Escalating regional tensions leading to higher military costs.

Global economic slowdown affecting exports.

Domestic political instability delaying reforms.

Positive catalysts include tech sector resilience and international partnerships.

Disclaimer: This news report is for informational purposes only and does not constitute financial advice or investment tips. Sources are not mentioned.