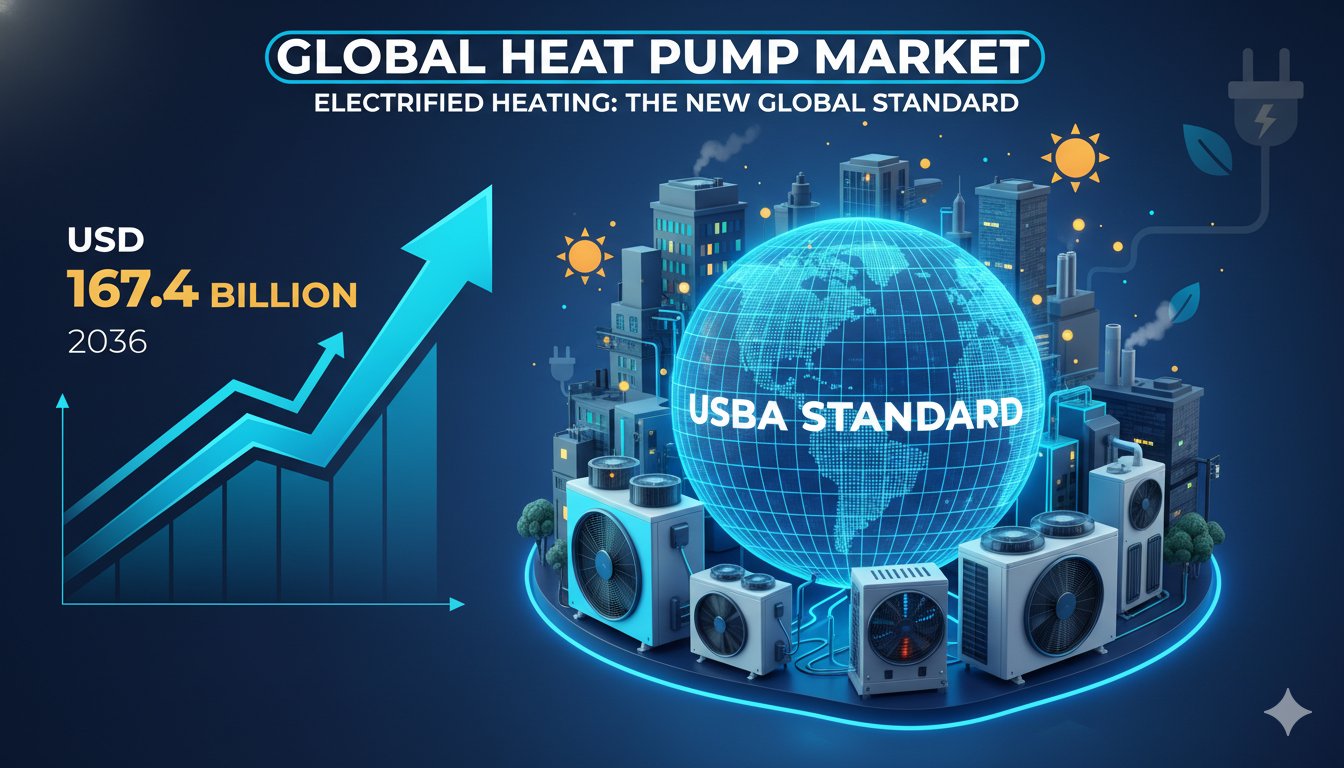

“The global heat pump market stands at USD 61.7 billion in 2026 and is projected to surge to USD 167.4 billion by 2036, achieving a compound annual growth rate of 10.5 percent, fueled by widespread adoption of electrified heating systems, stringent energy efficiency mandates, and the accelerating transition from fossil fuel-based solutions. Dominant segments feature air-to-air technologies holding a 46.1 percent share and residential end-users commanding 55.3 percent, with natural refrigerants gaining traction at 22.7 percent amid regulatory pressures for low-global-warming-potential alternatives.”

The push toward electrified heating is reshaping energy consumption patterns worldwide, with heat pumps emerging as a cornerstone technology for reducing carbon footprints in buildings. These systems, which efficiently transfer heat rather than generate it through combustion, are increasingly integrated into new constructions and retrofits, offering dual functionality for heating and cooling. Market expansion is particularly pronounced in sectors where energy costs and environmental compliance are critical, as utilities and governments roll out incentives to spur adoption.

Advancements in inverter-driven compressors and smart controls have enhanced system reliability, allowing for seamless operation across varying loads and temperatures. This has broadened applicability, from single-family homes to large-scale commercial facilities, where heat pumps now compete directly with traditional boilers and furnaces. The market’s trajectory reflects a broader shift in energy policy, emphasizing resilience against volatile fuel prices and alignment with net-zero goals.

Market Segmentation and Key Metrics

Heat pumps are categorized by technology, refrigerant type, end-user application, and power capacity, each revealing distinct growth dynamics.

By technology, air-to-air systems dominate due to their affordability and ease of installation, capturing nearly half the market. These units excel in moderate climates, providing efficient space heating and air conditioning through ducted or ductless configurations. Air-to-water variants follow closely, favored in hydronic systems for underfloor heating and hot water supply, while ground-source options, though higher in upfront costs, deliver superior long-term efficiency by leveraging stable underground temperatures.

Refrigerant segmentation highlights a transition toward eco-friendly options. Hydrofluorocarbons still hold sway but are yielding to natural refrigerants like carbon dioxide and hydrocarbons, which minimize environmental impact. Hydrofluoroolefins represent an emerging category, balancing performance with lower global warming potential to meet evolving standards.

End-user breakdown underscores residential dominance, where homeowners seek cost savings on utility bills amid rising energy prices. Commercial applications, including offices and retail spaces, prioritize scalability and integration with building management systems. Industrial uses, though smaller, are growing in processes requiring precise temperature control, such as food processing and manufacturing.

Power capacity segments include small-scale units under 10 tons for homes, medium-scale for mid-sized buildings, and large-scale for expansive facilities. Small-scale leads in volume, driven by suburban and urban housing booms.

| Segment | 2026 Market Share (%) | Projected 2036 Value (USD Billion) | CAGR (2026-2036) |

|---|---|---|---|

| Air-to-Air Technology | 46.1 | 77.2 | 10.7 |

| Residential End-User | 55.3 | 92.5 | 10.6 |

| Natural Refrigerants | 22.7 | 38.0 | 11.2 |

| Small-Scale Capacity | 48.5 | 81.2 | 10.4 |

These metrics illustrate how targeted innovations are propelling specific areas faster than the overall market average.

Growth Drivers Propelling Market Expansion

Electrification mandates are a primary catalyst, as jurisdictions enforce bans on new fossil fuel installations in buildings. This regulatory landscape compels builders and property owners to opt for heat pumps, which align with carbon reduction targets by leveraging renewable electricity sources. Utility rebate programs further lower barriers, offering cash incentives that offset installation expenses and accelerate payback periods.

Energy efficiency regulations play a pivotal role, with standards requiring higher seasonal performance factors that heat pumps readily achieve—often exceeding 300 percent efficiency compared to 90 percent for gas furnaces. The replacement cycle of aging heating infrastructure amplifies this, as millions of outdated systems are phased out in favor of modern, electrified alternatives.

Technological strides in cold-climate performance have unlocked new geographies, where variable-speed compressors maintain output even in sub-zero conditions. Integration with solar panels and battery storage enhances self-sufficiency, reducing grid reliance and operational costs. Rising awareness of indoor air quality benefits, such as reduced emissions and better humidity control, also boosts consumer appeal.

Economic factors, including fluctuating natural gas prices, make heat pumps a hedge against volatility, with lifetime savings often surpassing initial investments. Corporate sustainability commitments drive commercial uptake, as businesses incorporate these systems into ESG strategies to attract eco-conscious stakeholders.

Regional Insights and Geographic Dynamics

North America, led by the United States and Canada, is witnessing accelerated growth through federal tax credits and state-level initiatives that subsidize transitions from oil and gas heating. In the U.S., policies encourage widespread deployment in both new builds and existing structures, particularly in the Northeast and Midwest where heating demands are high. Canada’s focus on rebates and retrofit programs addresses its colder regions, fostering innovation in resilient designs.

Europe stands out for its aggressive decarbonization agenda, with countries like Germany and France implementing building renovation waves. Germany’s high CAGR stems from funding schemes that prioritize electrification, while France emphasizes affordability through grants for low-income households. The region’s emphasis on district heating networks integrated with heat pumps amplifies scale efficiencies.

Asia Pacific emerges as a high-volume growth engine, driven by urbanization in China and Japan. Japan’s market thrives on compact, efficient units suited to dense urban environments, with government support for energy conservation. Emerging economies in the region are adopting heat pumps for cooling-dominant needs, transitioning from less efficient air conditioners.

Other regions, including Latin America and the Middle East, show nascent potential as awareness grows, though challenges like infrastructure limitations temper pace.

| Region/Country | 2026 Market Value (USD Billion) | 2036 Projected Value (USD Billion) | CAGR (2026-2036) |

|---|---|---|---|

| United States | 12.3 | 31.5 | 10.2 |

| Canada | 4.1 | 10.3 | 10.6 |

| Germany | 5.8 | 15.9 | 12.1 |

| France | 3.9 | 9.8 | 10.9 |

| Japan | 7.2 | 18.7 | 11.8 |

| Asia Pacific (Overall) | 18.5 | 50.2 | 10.5 |

This table highlights how policy frameworks influence regional variances, with Europe outpacing others in growth rates.

Competitive Landscape and Industry Players

The market features a mix of established giants and innovative specialists, competing on efficiency, durability, and service ecosystems. Leading firms invest heavily in R&D to refine compressor technologies and expand refrigerant portfolios, often through acquisitions and partnerships.

Strategic moves include vertical integration to control supply chains for components like heat exchangers and sensors, ensuring cost competitiveness. Collaborations with utilities and governments enable pilot programs that demonstrate real-world performance, building trust among installers and end-users.

Market share is consolidated among top players, but niche entrants focus on specialized applications, such as high-temperature industrial pumps or ultra-quiet residential models. Global expansion strategies target high-growth regions, with localized manufacturing reducing logistics costs and tariffs.

Technological Advancements Shaping the Future

Innovations in smart connectivity allow heat pumps to interface with home automation platforms, optimizing operation based on occupancy, weather forecasts, and electricity tariffs. Predictive maintenance algorithms use IoT sensors to preempt failures, minimizing downtime and extending equipment life.

Hybrid systems combining heat pumps with gas backups provide redundancy in extreme conditions, appealing to risk-averse markets. Advances in geothermal drilling techniques lower installation hurdles for ground-source variants, making them viable for urban settings.

Refrigerant research emphasizes safety and efficiency, with blends that maintain performance while slashing environmental impact. Energy storage integration, via thermal batteries, smooths demand peaks, enhancing grid stability and enabling off-peak operation for cost savings.

Challenges and Strategic Opportunities

Upfront costs remain a hurdle, particularly for retrofits involving system upgrades like enhanced insulation or larger distribution networks. Addressing this requires financing models, such as heat-as-a-service, where users pay monthly fees covering installation and maintenance.

Workforce shortages in skilled technicians necessitate expanded training programs to ensure proper sizing and commissioning, which directly impact efficiency outcomes. Cold-climate skepticism persists, though field data from recent deployments shows consistent performance improvements.

Opportunities lie in emerging applications, like data centers and electric vehicle charging hubs, where waste heat recovery via pumps boosts overall site efficiency. Policy evolution offers tailwinds, as incentives evolve to cover advanced features like demand response capabilities.

The market’s resilience is evident in its adaptation to supply chain disruptions, with diversified sourcing ensuring steady component availability.

Disclaimer: This news report provides informational insights and tips based on industry analyses and sources, but it is not intended as financial advice or investment recommendations.